What does my home cost to run each week?

05 Dec, 2021

Since I wrote Are you scared of NOT buying a house a few months back, I’ve had a lot of feedback. That post had the desired effect; I wanted people who are renting to feel happy about their decision to rent. Plus, I wanted you to see that there are ways to become financially independent outside of homeownership.

Today’s blog post is a follow on for all the non-homeowners who told me that they were curious about the expenses I incur for my own home, which you are missing out on by renting. There are a lot more expenses than just paying your mortgage. Knowing what owning a house costs ME might help you plan your future house purchase or make you even happier renting than you already were.

For this blog post, let’s put our rose-tinted glasses on and assume that you are living in a nice, warm, dry rental property, with fair and stable rent that you can afford, flatmates who are awesome (or a space all of your own) and a landlord who respects you as a tenant. AKA is renting nirvana!

It’s not a foregone conclusion that you need to buy a home

In many situations, doing so could easily jeopardise your finances, not improve them, and for many, it just does not fit with the stage of life, lifestyle or career, to buy a house. A couple of people who are renting have specifically asked me for a breakdown of what it costs to run my home. Tim has emailed a list of questions which I will answer below, plus he also sent this Maintenance Schedule for a homeowner - YIKES - which managed to make the To-Do list for my whare that much longer!

Q. How do you weigh up doing work yourself (DIY) or hiring someone to do it for you?

Our house is eight years old, so it is in very good condition, but only because it's well built and we take good care of it. It’s a three-bedroom, two-bathroom home and about 175m2 in total (including garaging). Keeping the maintenance up to it is crucial because Central Otago summers and winters are brutal and can take their toll. Every summer, we repaint a few sides of our whare, and we are constantly working our way around it. Jonny is about to buy yet another 10L pail of stain for $150. It would not cross our minds to pay someone to do this for us because we have the time and the skills to do it.

Our house is of an age now where we are also doing some internal painting to refresh it. It’s not expensive; it just takes our time. We have also updated the wallpaper, curtains and furniture in a few rooms. Wallpapering was a first for us, and we did briefly consider paying someone to do it, but with a bit of a google tutorial, we gave it a go. And it worked out just fine!

Even when we built the studio in the yard for me to write this blog from, we just did our research and decided we could build it ourselves. Tradies are so busy at the moment, and they wouldn’t want to waste their time on such a small project anyway. It’s handy that I’ve married someone handy, and Jonny would say the same thing!

Q. What things do you wish you'd thought about and budgeted for?

We are both quite practical, and we also have the time to fix most things ourselves when they wear out or break. We know where our skills end, though, and in the past, we have called in a plumber to work on our central heating and solar hot water and an appliance repairer to fix our washing machine, fridge and freezer. In the eight years, we have lived here, we have replaced most of our major appliances.

We have since decided that there is no point in buying fancy brands. Paying more is no guarantee that they will last! Currently, our oven is on the blink, so that's another $1,000 soon to be spent! If there were anything worth setting up a budget for, it would probably be for replacing appliances, as we are surprised at how often they fail.

I think that new homeowners should always keep some money held back in an emergency fund. An “appliance budget” might be handy too! Because we know appliances keep breaking, we would (and have) happily used good second-hand cheaper appliances if we can find them.

Q. Are there hidden costs around fixing things? Also, how long does it take to fix things?

Back to the appliances again. Unfortunately, it’s a sad state of affairs that it costs more to fix an appliance than buy a new one. Ken, the local appliance repairman, is a top bloke, super smart, and if he can fix it, he will. But more than once, he has looked at a broken appliance and said, “just replace it”. By the time we paid his call-out fee AND purchased the new appliance, the costs had mounted up.

Another maintenance surprise is all of the rubber seals on our windows and doors. With the cold and the heat here, they contract, meaning they don’t seal as they should. I have to be honest here; this one is in the too hard basket for this year at least! But I suspect with the right tool and supply of rubber seals; we could do this ourselves.

Q. What didn't you think you'd need to maintain on your house? Any surprises?

Our section is 900m2 and mostly garden, but it cost very little money to create. We propagated many of our plants or bought small cheap ones and built our soil from cardboard, leaf litter and manure. BUT it does take a tonne of mahi (work) to keep it all under control. I subscribe to the “chaos” method of gardening, meaning that there is not a single straight garden bed in the place. And if a weed has a nice flower, well, it gets to stay. So, that is probably one of the unintended surprises of homeownership, just how many hours we spend each week taming the garden. At the risk of sounding like a boring middle-aged person, I’ve created some fantastic outside areas to spend time in and it currently all feels worthwhile.

A nice place to sit in the summer under the shade of our hops plant.

We are home a lot!

Our home gets 24-hour use, given that Jonny works from home and I’m here during the day a lot as well. So, due to the nature of our work being online, our internet costs are pretty high, plus we heat the house 24/7 too, and we feel these heating costs in our budget in the winter months.

Our biggest saving is?

Many years ago, we made becoming mortgage-free our priority and in our late 20’s and early 30’s we aggressively paid off our first home (we are now in our second). Having no mortgage payments heading out the door makes a massive difference to our budget. But if we did have a $500,000 mortgage, we would have minimum payments of $3,658 per month (3.84% on a 15-year loan). That’s $914 a week, a huge drain on any income, and if we had to incur that cost as homeowners, both Jonny and I would need to completely change our lifestyle and pick up full-time work. I always advocate becoming debt-free ASAP.

Q. What maintenance you might need to budget?

As for budgeting for repairs, I don’t have a specific bank account (sinking fund) where I set money aside. If a repair comes up, I just pay for it out of our daily account. But I do have an annual budget for it in PocketSmith to keep track of what maintenance is costing us, and this year I allowed $1,800, which we have just exceeded. It’s an eclectic mix of expenses, too; plants, paint, curtains, new bedding, salt for the water softener and a regular plumbing checkup on our central heating system. Anything that goes in the house or garden, fixes the house, or makes the house look better, goes into that budget.

A lot of our ‘repairs’ are just updates, really, but you do need to keep this in mind because we all get sick of looking at the same four walls after a while. Curtains are a hidden cost of home maintenance and something to look out for. Put simply, they cost a fecking fortune, particularly when you need to have good thick drapes to keep out either the heat or the cold. I’ve either sewn our curtains or picked up high-quality second-hand ones to cut these costs. In the case of our living room curtains, how lucky am I to have found these retro gems for $20! The answer: VERY!

Second-hand $20 retro curtains.

Resale Value

The biggest expense for any homeowner is the dreaded words: Resale Value.

Too many people justify overspending on their homes because of resale value. Instead of making their home just the way THEY like it, they instead try to create a buyers paradise for some fictional futuristic person whose tastes they just don’t know. It is easy to overspend when you are designing someone else’s home. But it’s actually YOUR home right now.

Given that we only ever built our house with us in mind, the phrase “this will be good for resale value” never entered our minds. I think we have spent a lot less as a result. For example, we were urged by many to build a four-bedroom home instead of three. Huge additional upfront cost to us and we have never needed that extra space in the eight years we have lived here.

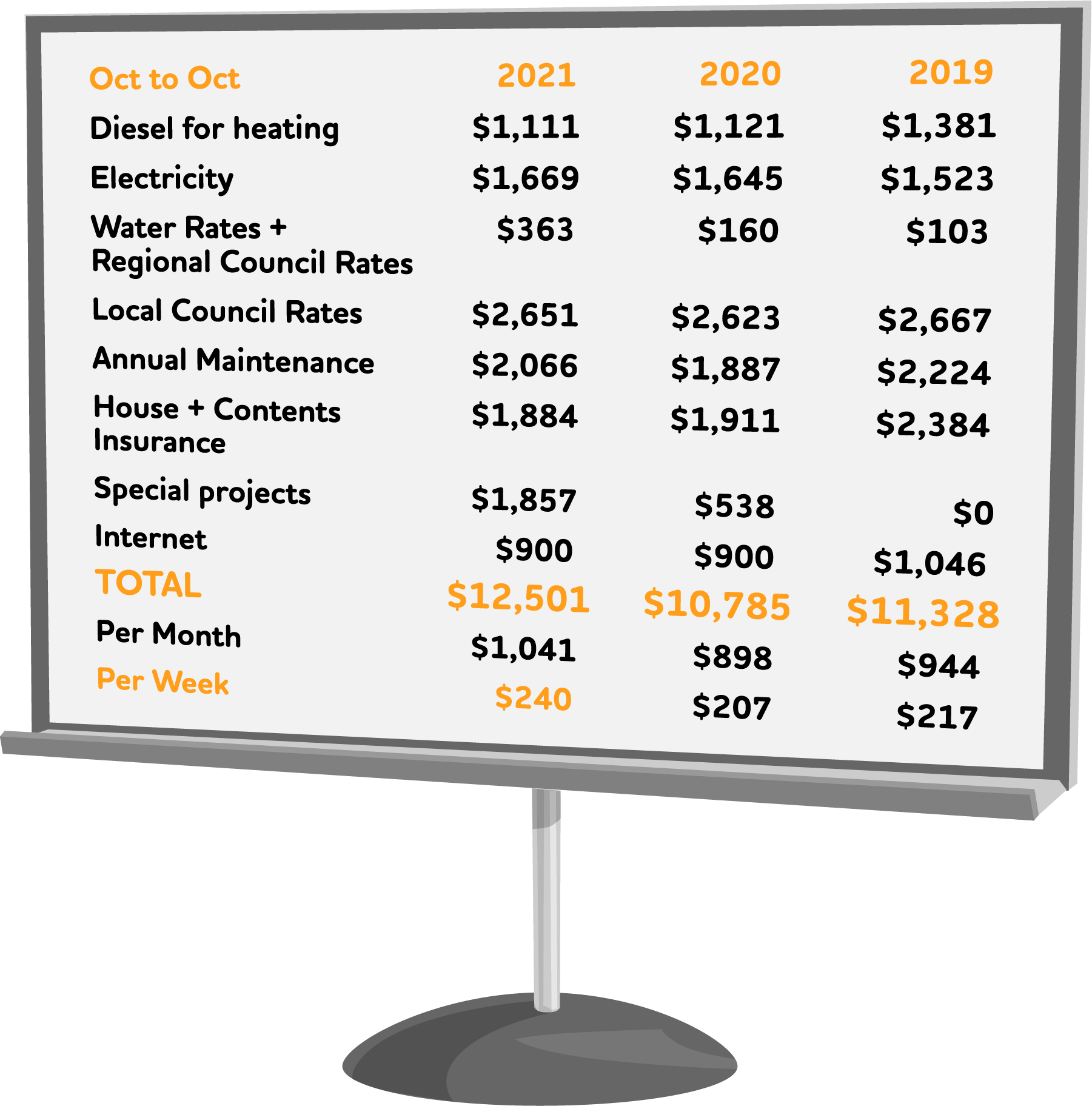

The numbers are in…

Thanks to PocketSmith I have the exact figures I need to work out my house-related costs and I’ve detailed them for the previous three years:

* The special project was my writing studio and a few other minor things

My housing costs are $240 per week

In 2021, owning our home costs us $240 each week, ever so slightly up from the previous years and this is an accurate breakdown of our exact costs.

Some expenses will be similar to yours, but some are unique to the homeowner. How does that compare to the rent you pay each week and all of your house-related outgoings? If you make $1,000 a week, what percentage of your paycheque is going on housing?

What’s leftover?

More importantly, what are you doing with that leftover money?

This is where those who rent have the jump over those who own. With no mortgage payments, and no money going to the upkeep of the whare, you get to keep more of your income.

How fast could you grow your wealth if you use this money to invest in your KiwiSaver and just a couple of low fee index funds? Homeowners are not the only people who get to enjoy capital gains, those who invest do too. In fact, over time, the share market outperforms the housing market and is far less faffing about.

If you read books such as Quit Like a Millionaire, this is exactly how Kristy and Bryce managed to retire at the age of 30. They rented and kept all housing-related and lifestyle costs as low as possible. Using the remainder of their incomes, they invested aggressively into index funds until they reached their FI number (25x their annual expenses invested into assets that return them an income). Their urge to buy a house was strong, there was a lot of pressure to do so, but doing so actually didn’t suit their lifestyle; they just couldn’t make the math stack up and instead continued to invest in the share market.

Rent any home you want, anywhere you want.

How FREE and agile will you feel knowing that renting gives you the option to change up where you live when you want to? To have the majority of your income available to you to invest in the share market, in assets that receive capital gains and pay dividends. People who ‘own’ their home with a mortgage run out of cash to invest and this is precisely how they become ‘house rich, cash poor’. Their home may have gone up in value, but they can’t ‘realise’ this value until they sell their home. Your home never pays you a dividend, and as my numbers show, it costs money every week to run it.

I’m not saying “never buy a home”, but I am saying that while you are choosing not to buy a home, you have a big chunk of your pay available to invest. If, at some later date, you buy a home, then good for you. Money gives you options. But, there are so many examples in the FIRE community of people who have become financially independent without owning their own homes. Start googling!

Invest all excess income; don’t spend it.

Throwing your hands up in the air and saying, “poor me, I can’t buy a house”, is not an option. Throwing your hands up in the air and saying, “go me, I’m investing $400 a week into a low fee broad-based index fund/ETF” certainly is! Grow your wealth that way instead, without the cost and hassle of owning property.

Because Aotearoa is so top-heavy in homeownership, it’s hard for people to see another way to grow their wealth. But I’m telling you that it is there.

Companies such as those listed below give you the vehicle to easily and cheaply invest in the share market. But please don’t pick stocks. Do your research and invest in just a couple of low fee broad-based index funds or ETFs and then just add to them on a weekly or monthly basis, consistently, never stopping: Sharesies, Kernel, Hatch, InvestNow, Smartshares

I know the rental market is tough out there, with a lot of issues. Still, I’m also fortunate to meet many decent landlords who are in it to provide a nice home. If you can find one of those, you can get stability in your renting situation, then get the rest of your income working for you. Build up your investments to tens of thousands, hundreds of thousands and then millions of dollars. The returns on that chunk of money will let you live in any rental you want, anywhere you want.

That’s freedom right there.

In fact, if we sold up our own home today, added it to the investments we already have in the share market and rented instead, we would be able to FIRE tomorrow.

Now to convince Jonny!

Happy Saving!

Ruth

A good follow on blog post to read is this one by Sonnie Bailey: Can’t afford a home in the current property market? You can still get into a good long-term financial position.